With rising demand from expats, professionals, and digital nomads, Singapore’s rental market remains strong in 2025. But not all areas are created equal — savvy landlords know that location, accessibility, and lifestyle appeal play a huge role in rental yield.

If you’re investing for passive income, here are the top districts in Singapore to watch closely this year:

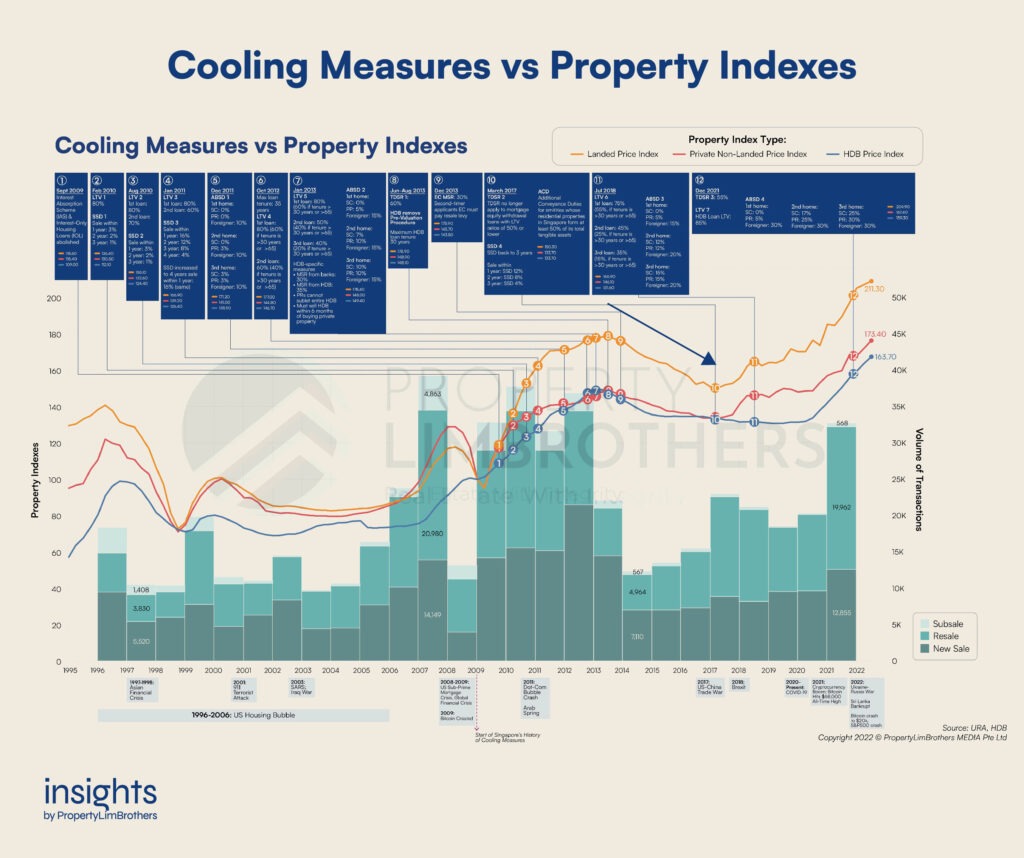

1. Additional Buyer’s Stamp Duty (ABSD)

This is the biggest cost factor for non-first-time or foreign buyers. Here’s the ABSD rate (as of 2025):

| Buyer Type | ABSD Rate |

| Singapore Citizen (1st home) | 0% |

| Singapore Citizen (2nd) | 20% |

| Singapore PR (1st home) | 5% |

| Foreign Buyer | 60% |

| Entities / Companies | 65% |

2. Total Debt Servicing Ratio (TDSR)

TDSR caps your total debt obligations (including mortgage) to 55% of your gross monthly income. This limits loan approvals and ensures financial prudence. This applies to both locals and foreigners applying for a bank loan in Singapore.

3. Loan-to-Value (LTV) Limits

How much loan you can get depends on your existing mortgage status:

- First loan: Up to 75%

- Second loan: Up to 45%

- Third loan: Up to 35%

This affects your cash/down payment, especially for second properties.

4. Seller’s Stamp Duty (SSD)

Sell your property within 3 years of purchase and you’ll be taxed:

- Year 1: 12%

- Year 2: 8%

- Year 3: 4%

This discourages quick flipping and short-term speculation.

Conclusion

While cooling measures may sound restrictive, they’re designed to keep Singapore’s real estate market safe, credible, and long-term investor-friendly. As a buyer or promoter, understanding these rules helps you better position your listings and guide your audience ethically.

Want to promote Singapore listings wisely? Focus on 1st-time buyer homes or properties with long-term value.